And they just got a 56% pay rise.

Here is the conversation nobody in iGaming is having honestly.

Consider a scene that industry insiders describe, in slightly different versions, again and again — a composite, but a faithful one. In 2025, a sportsbook operator quietly restructured its trading floor. Fifteen junior odds compilers were let go. Not because the company deployed a robot. Because three senior traders who had spent six months learning to use AI pricing tools could now do the work of eighteen. The three stayed. The fifteen left. The company’s trading accuracy improved. Costs dropped. Nobody issued a press release.

That story — with different numbers, different job titles, different cities — is playing out across the iGaming industry right now. In Malta. In Gibraltar. In Kyiv. In the content farms of the Philippines and the customer support centres of Romania. And the reason most people in the industry are not prepared for it is because the public conversation has been framed around the wrong threat.

The threat is not artificial intelligence replacing human intelligence.

The threat is AI-augmented humans replacing non-AI-augmented humans. One person with the right tools is doing the work of three people without them — and earning more while doing it. The disruption is not coming from the server farm. It is coming from the Tuesday afternoon training session where your colleague figured something out that you have not yet.

PwC’s 2025 Global AI Jobs Barometer quantified this dynamic in a way that should make every iGaming professional stop and re-read: workers with AI skills are already commanding a 56% wage premium over colleagues in equivalent roles who lack those skills — up from a 25% premium just twelve months earlier. And in PwC’s June 2026 update, that premium climbed again — to 62%, reaching as high as 118% in some sectors. The market is repricing human labour in real time. The gap is not closing. It is compounding.

This is the article about what that actually means for the people who build, run, and grow this industry.

The Trading Room: A Case Study in What Already Happened

To understand what is coming, look at what has already happened in the sports betting trading function. Because it happened faster and more completely than anyone publicly predicted — and it happened in a way that was invisible until it was done.

In 2019, a well-staffed sportsbook trading room looked like a dealing floor. Rows of analysts tracking live events, compiling pre-match odds from spreadsheets and data feeds, adjusting lines manually as market information came in. A junior odds compiler would spend their day pricing lower-league football matches — pulling historical data, applying house margin, comparing against the market, and submitting their numbers for review. It was slow, human, and expensive.

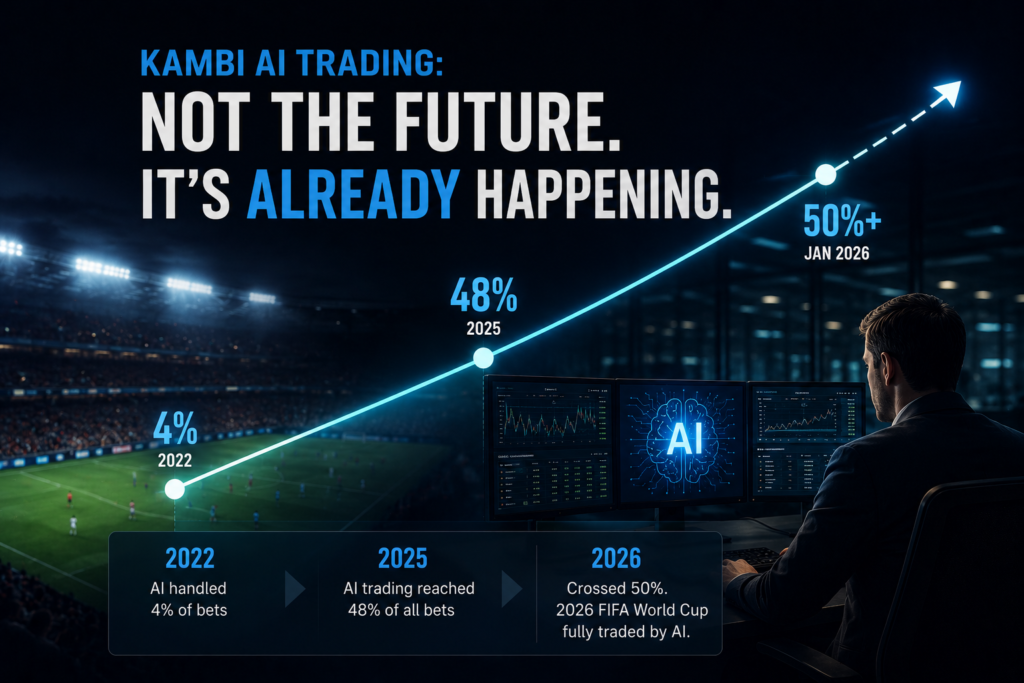

In 2022, Kambi — one of the industry’s leading sportsbook technology providers — launched AI trading for the FIFA World Cup. At launch, AI handled 4% of bets on its network.

By 2025 — three years later — AI was trading 48% of all bets on Kambi’s network. Up from 4% to 48% in thirty-six months.

That is not a statistic about the future. It is a statistic about what already happened. And since then, the question of how quickly the remaining half would follow has already begun answering itself: in its February 2026 earnings call, Kambi confirmed it crossed the 50% tipping point in January 2026 — and stated that the 2026 FIFA World Cup will be the first major global tournament fully traded by AI across its network. Kambi’s own technology page describes AI trading as elevating odds creation through the pricing and trading of odds without human intervention. The trajectory is unambiguous.

The junior odds compiler whose job was to price lower-league football markets using historical data and a house margin model? That role is not threatened. It is already gone. What remains in the trading room is a smaller group of senior professionals doing something qualitatively different: supervising the AI’s output, managing edge cases the model cannot handle, detecting unusual patterns that suggest match manipulation, and making judgment calls that require regulatory knowledge and experience rather than data processing. These are people who understand AI well enough to know when it is wrong. And they are paid accordingly.

The trading room did not close. It got smaller, smarter, and more expensive per head. That is the template for what happens next across the rest of the industry.

The Support Floor: The Largest Single Disruption in iGaming Employment

Customer support is the biggest employer in the iGaming operator stack. A mid-sized operator running across multiple markets might employ two hundred to five hundred support agents handling deposits, withdrawals, bonus queries, account verification, and the thousand variations of “why can’t I log in.”

It is also, structurally, the most exposed function in the industry to AI replacement. Not because the people doing it are unskilled — they are not — but because the work is exactly the kind AI does best: high-volume, rule-based, repeatable, and predictable.

The macro evidence for what is happening is already documented outside iGaming in numbers too large to dismiss. Klarna deployed an AI customer service system in 2024 and reported it handled the equivalent work of 700 full-time agents in its first month while maintaining customer satisfaction scores. (Tellingly, Klarna later rehired human agents in 2025 for complex and sensitive cases — a course correction that confirms rather than contradicts the tiered model: AI absorbs the volume, humans keep the judgment calls.) Salesforce cut roughly 4,000 customer support roles — from 9,000 heads to about 5,000, in CEO Marc Benioff’s own words — as its Agentforce AI platform absorbed the routine interaction load. By early 2025, 98% of contact centres globally had adopted AI in some form.

Inside iGaming, the shift is being driven by platforms explicitly built for this purpose. BetHarmony — a conversational AI product designed for sportsbook and casino operators — is marketed specifically as a replacement for overloaded queues and costly conversion gaps, handling player queries, bet placement support, and account management through voice and chat without human involvement. The economics for operators are not subtle: AI support costs a fraction of a human team, is available 24 hours a day in any language, and scales instantly when a Champions League quarter-final kicks off at 8pm on a Tuesday.

This does not mean every support agent is redundant. It means the tier-1 support agent — the one handling the FAQ-level query that comprises the vast majority of daily contact volume — is redundant. What remains is a smaller, higher-skilled team handling the conversations that AI genuinely cannot: complex disputes, gambling harm disclosures, VIP relationship management, regulatory escalations. These conversations require human judgment, emotional intelligence, and legal awareness. They also represent perhaps 15–20% of total support volume.

The mathematics are uncomfortable. An operator with 300 support agents today may need 50 to 60 in 2030 — plus one or two “AI Oversight Specialists” who monitor chatbot performance, train the system on new edge cases, and manage quality. The 50 remaining will earn more. The 240 who left will need to find something else.

The Content Farm: The Disruption That Already Happened

The affiliate content industry in iGaming was, for fifteen years, one of the most reliable employment generators the industry had. Hundreds of websites, thousands of writers, churning out casino reviews, slot game descriptions, sportsbook bonus comparisons, and “best casino in [country]” roundup articles for global SEO distribution.

It is over. Not coming to an end. Over. The model is structurally broken and the evidence is sitting in the public financial statements of the industry’s largest affiliates.

Catena Media — once generating €76.7 million in annual revenue from content-driven affiliate traffic — reported a 35% revenue collapse to €49.6 million by 2024. Better Collective saw revenue fall 18% year-on-year in Q2 2025. Catena Media explicitly cited Google’s algorithm updates — the “helpful content” changes that specifically targeted thin, keyword-optimised content produced at scale and replaced it in search rankings with authoritative, experience-based, genuinely expert writing. Better Collective’s decline had additional drivers, including Brazil’s regulatory transition, but the structural pressure squeezing the entire content-affiliate model is the same.

Here is the thing about AI’s role in this: it ran in both directions simultaneously. AI tools made it trivially easy to produce generic casino review content at infinite scale — which created a flood of low-quality content that trained Google to penalise it, which destroyed the SEO business model that employed thousands of writers to produce it, which collapsed the revenue of the companies that employed them. AI broke the market it was helping to serve.

What is growing in its place is something more difficult, less scalable, and significantly more valuable: genuine iGaming journalism and analysis. The kind of article that requires actual industry knowledge, real source relationships, original data, and a point of view. The kind of content that AI cannot produce because it requires being inside the industry, talking to people, forming opinions, and being wrong in public and corrected.

The content role that survives 2030 in iGaming is not “writer who can produce 10 casino reviews per day.” It is “analyst-journalist who understands the industry well enough to write something that operators and regulators actually want to read.” These people are rare. They are well-compensated. And there are not enough of them.

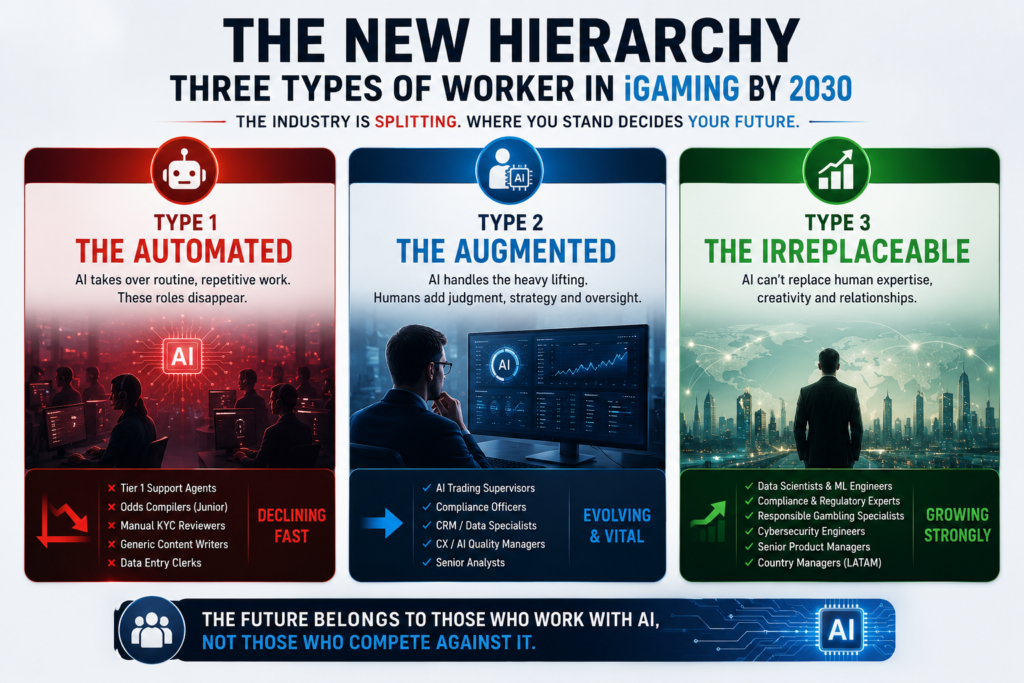

The New Hierarchy: Three Types of Worker in iGaming by 2030

All of this collapses into a framework that is simpler — and more actionable — than the standard “disappearing/thriving” categorisation. By 2030, every person working in iGaming will sit in one of three categories. The category is not determined by their job title. It is determined by their relationship to AI.

Type 1: The Automated

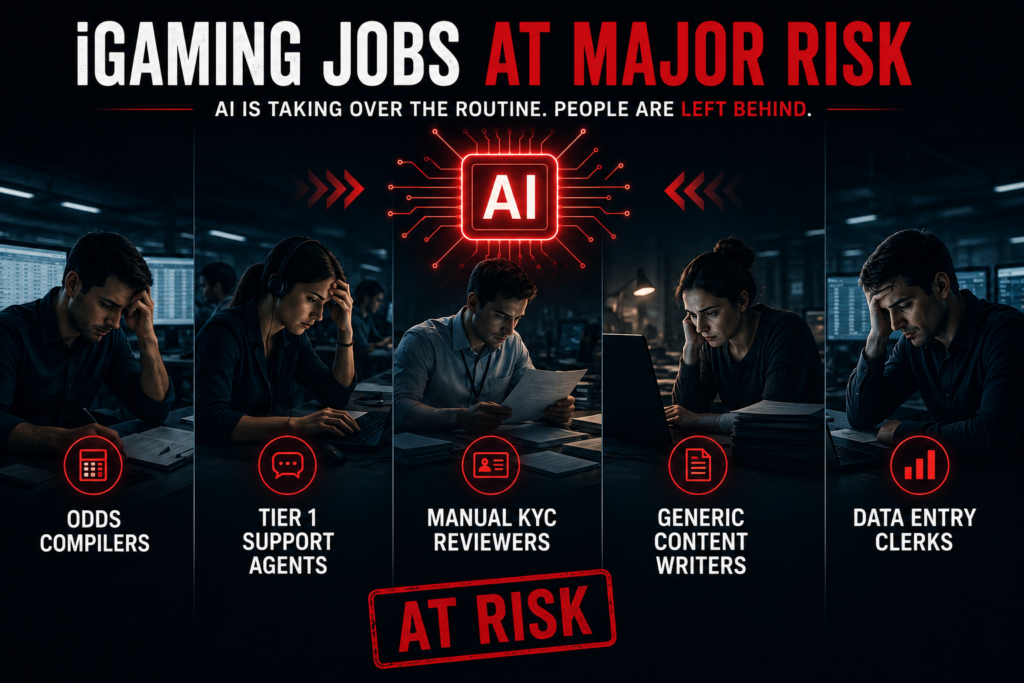

These are roles where the primary function has been taken over by AI systems, leaving no structural need for the human to perform it.

The entry-level customer support agent routing queries and answering FAQ-level questions. The odds compiler pricing standard pre-match markets from historical data. The manual KYC reviewer checking document authenticity against player registrations. The content writer producing templated game descriptions and bonus comparison pages.

The jobs still exist in 2026 — but the clock is visible. AI already handles more than half of the trading function on the industry’s most transparent network. Didit’s automated KYC system delivers onboarding in 25 seconds with a 60% reduction in manual review. AI chatbots are closing in on handling the majority of first-contact support queries. The question for everyone in this category is not whether the function will be automated. It is whether that happens before or after they have built skills that move them into the next category.

Type 2: The Augmented

This is the largest and most important category — the roles that will still exist in 2030, but which will look completely different, employ fewer people, and require fundamentally different skills from today’s incumbents.

The senior trading analyst whose job shifts from pricing creation to AI model supervision and integrity oversight. The compliance officer who must now understand regulatory API architecture well enough to specify automated compliance systems. The CRM manager whose campaign-building function gives way to a personalisation data science function. The customer experience specialist who manages AI chatbot performance rather than handling conversations directly.

These roles are not going away. In fact, they are growing in total remuneration and strategic importance. But the version that exists today is being replaced by a version that requires genuine technical literacy, data fluency, and the ability to work alongside and supervise AI systems.

The most dangerous position in iGaming right now is being a competent performer in a Type 2 role without any urgency about developing the skills the augmented version of that role requires. Because the augmented version is being staffed — right now, today — with people who already have those skills.

Type 3: The Irreplaceable

These are the roles that AI has made more valuable rather than less — because the scarcity of the skills they require increases as the automated layer of the workforce grows.

Data Scientists and ML Engineers. AI/ML job postings increased 163% in 2025 versus 2024. Employment of data scientists is projected to grow 34% through 2034. In iGaming, the applications multiply constantly: churn prediction, fraud detection, personalisation engines, responsible gambling monitoring systems, pricing model validation.

Compliance and Regulatory Affairs Specialists. The regulatory landscape in iGaming is not simplifying — it is compounding. As we documented in our iGaming License Guide 2026, every major market is adding new requirements simultaneously. Brazil launched a full regulatory framework in January 2025. The Netherlands moved to 37.8% GGR tax. Germany, Sweden, Romania, the Czech Republic — all adding compliance strings. These people cannot be automated because their value lies in judgment — regulatory interpretation, relationship management with licensing bodies, strategic advice on market entry.

Responsible Gambling Specialists. Global gambling industry regulatory fines totalled $184.4 million in 2024. Responsible Gambling Officers are not just in demand. In many jurisdictions, they are a licence condition.

Cybersecurity Engineers. iGaming fraud has doubled in two years. Deepfake attacks on KYC systems are a documented and growing threat. The people who secure these systems are among the most structurally protected professionals in the workforce.

Senior Product Managers. The iGaming operator of 2030 is a technology company. Flutter, bet365, DraftKings already operate with the engineering culture and product velocity of tech firms. The skill set — gambling domain expertise plus data literacy plus technical fluency plus regulatory awareness — does not exist in volume anywhere in the talent market.

The LATAM and Africa Opportunity: Where the New Jobs Are Being Created

While the automated layer shrinks in mature European markets, two regions are generating genuine net employment growth in iGaming — and understanding where the jobs are being created is as important as understanding where they are being eliminated.

Latin America — The Fastest-Growing iGaming Job Market in the World

LATAM iGaming salaries have essentially doubled in the past two years. Customer service representatives who were previously earning $600–800 per month are now commanding $1,500–2,000 plus bonuses, as operators compete aggressively for local talent with market knowledge.

As we analysed in our complete guide to iGaming in Latin America, the roles most in demand across Brazil, Argentina, Colombia, and Mexico are not the ones being automated — they are the ones that require local knowledge that cannot be outsourced or automated: country managers who understand local regulation and culture, VIP managers with relationship-based retention skills, legal advisors navigating complex and rapidly evolving local regulatory frameworks, and affiliate managers who understand the specific traffic sources and influencer culture of each country.

Brazil alone will generate thousands of compliance, marketing, payments, and product roles between now and 2030 as the newly regulated market matures.

Africa — Where iGaming Employment Is an Attractive Proposition

In African markets — where Super Group earns 37% EBITDA margins and the lottery sector alone represents a $5.6 billion industry, as we covered in our deep dive on the 5/90 lottery market — the jobs being created are predominantly operations, compliance, and customer-facing roles that require local language fluency and cultural knowledge.

The iGaming job market in Africa is genuinely different from Europe. The automation wave arrives more slowly in markets where labour costs are lower, regulatory requirements are less demanding, and where the human element of customer relationships carries disproportionate commercial weight. An African betting operator’s VIP relationship manager is not a role at risk of automation — they are often the primary reason a high-value player stays on the platform.

The Roles and What They Actually Pay in 2026

| Role | 2026 Salary Range | Demand | AI Threat |

| ML Engineer / Data Scientist | €70,000 – €130,000 | ↑↑↑ Growing fast | Negligible |

| Compliance / Regulatory Affairs | €60,000 – €110,000 | ↑↑↑ Growing fast | Very Low |

| Responsible Gambling Specialist | €45,000 – €80,000 | ↑↑ Growing | Very Low |

| Cybersecurity Engineer | €75,000 – €140,000 | ↑↑ Growing | Low |

| Senior Product Manager | €80,000 – €140,000 | ↑↑ Growing | Low |

| CRM / Personalisation Data Scientist | €65,000 – €110,000 | ↑↑↑ Growing fast | Negligible |

| LATAM Country Manager | $60,000 – $120,000 | ↑↑↑ Growing fast | Very Low |

| AI Trading Supervisor | €55,000 – €90,000 | ↑ Stable-growing | Low |

| Tier-1 Customer Support Agent | €18,000 – €30,000 | ↓↓↓ Declining fast | Extreme |

| Manual KYC Reviewer | €20,000 – €32,000 | ↓↓ Declining | Very High |

| Generic SEO Content Writer | €20,000 – €35,000 | ↓↓↓ Declining fast | Extreme |

| Entry-Level Odds Compiler | €25,000 – €38,000 | ↓↓↓ Declining fast | Extreme |

The Question Everyone in iGaming Should Be Asking Right Now

Not “will AI replace my job?” The framing is wrong. The more useful questions are:

Am I in a Type 1, Type 2, or Type 3 role right now? If Type 1, the clock is visible and the urgency is real. If Type 2, the question is whether you are building the augmented version of your skills or waiting to be replaced by someone who already did. If Type 3, the question is how you deepen the scarcity of your expertise — because scarcity is protection.

Is the person three desks from me doing my job better than me because of a tool I have not yet learned? This is the question that feels uncomfortable because the answer might be yes. And if it is yes, the appropriate response is not to feel threatened by that person — it is to have the conversation they have noticed you are not having yet.

What does the 2030 version of my role look like, and am I building toward it or toward an older version?

The Honest Conclusion

The iGaming industry is not heading toward an employment crisis at the macro level. The market is too large, growing too fast, and opening too many new geographies for total headcount to decline. But within the existing workforce, the disruption is structural, directional, and accelerating. The entry-level transactional layer is being automated out with a speed that the public conversation underestimates, because the companies doing it are not holding press conferences. They are just quietly restructuring and moving on.

The people who will thrive in iGaming in 2030 are not necessarily the people with the most experience. They are the people who most clearly understand which direction the industry is moving and are walking toward it rather than waiting to see what happens.

The person three desks from you has probably already started walking.

Related Reading

- The Hidden Economics of iGaming — Who Really Makes the Most Money?

- iGaming Latin America 2026 — The Complete Operator’s Guide

- iGaming License Guide 2026 — From €7,000 to €800,000

Sources

- PwC 2025 Global AI Jobs Barometer (56% wage premium)

- PwC 2026 Global AI Jobs Barometer (62% wage premium)

- Kambi 2025 Sports Betting Trends Report — 48% of bets AI-traded (NEXT.io)

- Kambi crosses 50% AI trading; 2026 World Cup fully AI-traded (Legal Sports Report)

- Klarna AI assistant — equivalent work of 700 agents (Klarna press release)

- Salesforce cuts ~4,000 support roles as AI steps in (Fortune)

- Catena Media FY2024: revenue down 35% to €49.6m (iGaming Future)

- Better Collective Q2 2025: revenue down 18% year-on-year (company announcement)